May 1, 2026

The $111 Billion Shrug

What happens when the best quarter in Apple’s history stops being exciting.

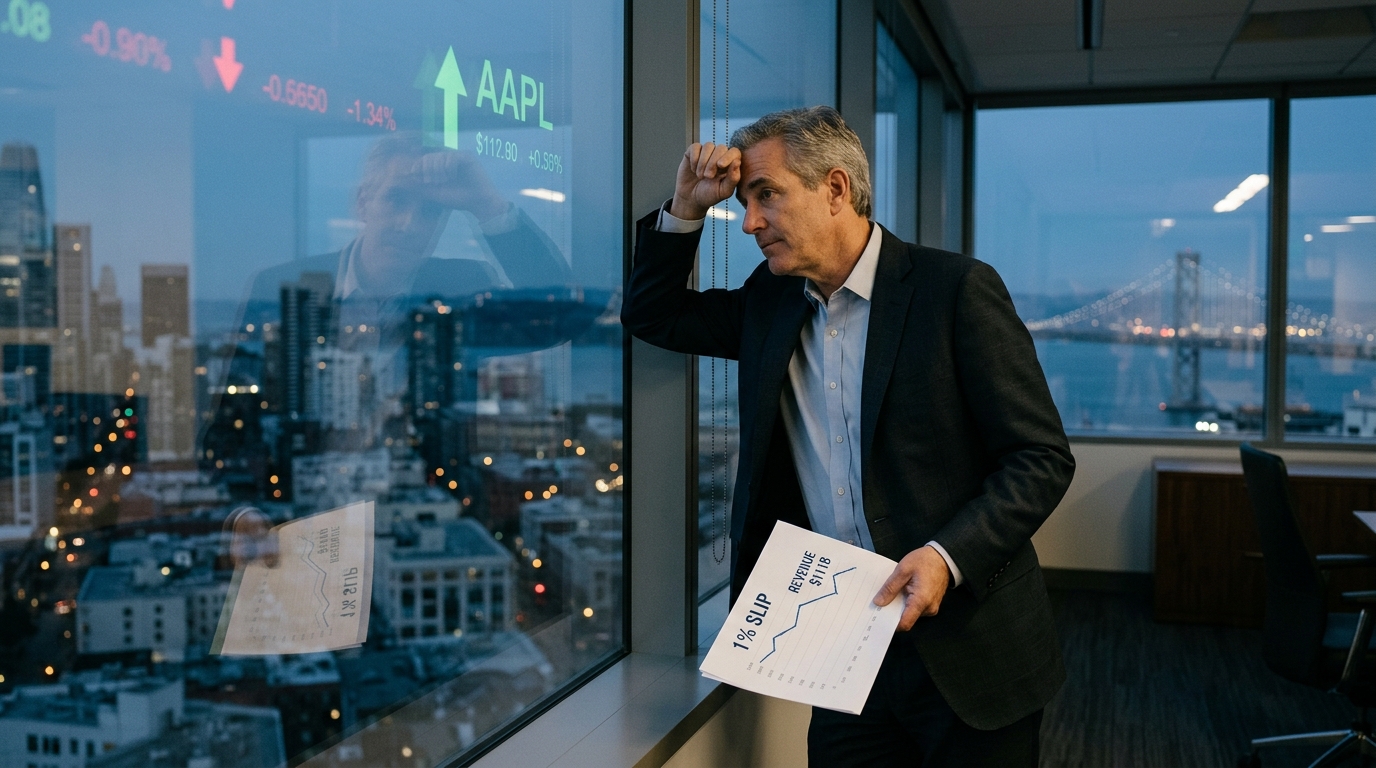

At some point last Thursday, Tim Cook finished an earnings call that any CEO in America would have traded their career for. $111 billion in revenue. Gross margins north of 49%. Services revenue at a record $30.98 billion. China up 28%. A $100 billion buyback. Forward guidance that doubled what analysts had modeled. And the stock? It drifted. Went slightly negative. Then came back maybe 2%.

Not a celebration. Not even a clean exhale. Just a shrug.

That reaction is more interesting than any of the numbers.

Your Free Options Book Is About to Vanish

In case you missed it… make sure you get your free “Simple Options Trading For Beginners” book before your link expires.

I eventually plan to charge money for this training, so do yourself a favor and download it now…

That way, no matter what it costs in the future, you’ll have a free copy.

Sound good?

Here is the actual problem with being Apple in 2026. Trailing twelve-month revenue is approaching $430 billion. To grow that number by 15%, you need to produce roughly $65 billion in new revenue in a single year. Not growth on top of a startup base. Growth on top of a base that is already larger than most countries’ GDP contributions from their entire technology sectors. The denominator is working against you at every turn, and no amount of operational excellence changes that math.

The $100 billion buyback, which sounds aggressive, is the tell here. When the most profitable consumer technology company in history cannot find a more productive use for $100 billion than buying back its own shares, that is not a sign of strength. It is a sign of saturation. Compare that posture to what Google, Amazon, and Microsoft are doing — each committing $100 billion or more into AI infrastructure this year, racing to build out capacity that does not yet have a fully defined revenue model but carries real option value. Alphabet rallied close to 10% this earnings season on Google Cloud’s 63% growth. Apple, with a cleaner scorecard on almost every traditional metric, moved a fraction of that. The market is not confused. It knows exactly what it is rewarding.

Worth mentioning: R&D spending jumped 33% this quarter to $11.42 billion. That acceleration is the most quietly significant number in the entire release. Either Apple is building something real in AI, or it is spending to catch up. The market has not decided which yet, and the Google Gemini partnership powering Siri does not exactly resolve the question. It raises it.

Add in the memory cost headwind Cook flagged — gross margin guidance for the June quarter compresses to 47.5–48.5% from 49.3% now, with the impact expected to grow beyond June — and you have a stock where the near-term setup is fine but not exciting, and the long-term setup depends on questions that do not have answers yet. Incoming CEO John Ternus takes over September 1. He inherits a flawless machine and an unanswered AI question. That is either a great job or a very hard one, depending on which way the next 18 months break.

Do NOT buy any SpaceX IPO shares until you see THIS

The filing positions the company for a June 2026 listing with a staggering valuation potentially exceeding $1.75 trillion.

But before you go out and load up on as much SpaceX shares as you can, know this:

Tech legend Michael Robinson says there’s a much better way to tap into this massive IPO windfall…without touching a single SpaceX share.

To see the details about this rare opportunity click here now.

So where does the capital go when the safe haven stops moving?

Some of it is finding Allogene Therapeutics (ALLO). The company is developing what it calls off-the-shelf CAR T therapies — cell therapies built from donor cells rather than the patient’s own, which solves a manufacturing problem that has kept CAR T from scaling. The pivotal ALPHA3 trial just posted interim data: 58.3% MRD clearance in the treatment arm against 16.7% in the observation arm. A 41.6% absolute difference. The clinical bar for meaningful efficacy is generally set at 25 to 30%. Allogene cleared it with room.

The company raised $200 million after that read, at $2.00 per share, and extended its cash runway into Q1 2028. The next catalyst is proof-of-concept data from the RESOLUTION trial of ALLO-329 in autoimmune disease, expected in June. That is a binary event in the truest sense — data either confirms the signal or it doesn’t, and the stock moves accordingly. For traders who specifically look for asymmetric setups ahead of hard catalysts, this is the profile. High uncertainty, defined timeline, clear outcome. Nothing like owning Apple at 34x earnings and waiting for something to happen.

GoDaddy (GDDY) is the other kind of interesting. No binary event. No clinical trial. Just a steady margin expansion story that most institutional desks are not modeling aggressively enough. Q1 2026: revenue of $1.3 billion, free cash flow of $474 million, EBITDA margin expanding 210 basis points to 33%, all at the high end of guidance. Full-year FCF target of $1.8 billion. The part people are skipping is the AI product velocity — an AI website builder hit $10 million in annualized bookings within weeks of beta launch, and an AI sales agent is handling thousands of customer interactions with, by the company’s own description, strong engagement and conversion. That kind of product-level AI integration compounds into retention before it ever shows up in a revenue line. The stock moved 4.7% on the quarter. The margin trajectory suggests there is more.

Watch Your Mailbox for Elon’s Weird Package

Look out for a package from Bastrop, Texas. It could arrive any day – and it’s from Elon Musk. It’s part of a project he’s waited 27 years to launch, which could be 15 times bigger than SpaceX, Tesla and xAI combined.

None of this is a knock on Apple. The business is genuinely excellent. Cook built something that will generate cash and return capital for years regardless of what the stock does in any given quarter. But there is a version of that excellence that becomes its own constraint — a company so optimized for the present that the market stops pricing in a future.

That is where AAPL sits right now. And the capital that came for growth, not income, is already somewhere else.