May 31, 2026

Copper and Uranium in 2026: Supply Still Feels Tight

A quick update with the newest numbers and a more careful read on what they do and do not prove

First a note from Stansberry Research

Dear Reader,

Something extraordinary is happening in the markets right now.

I’ve been watching the markets for nearly 20 years… And the data I’m looking at right now is unlike anything I’ve seen before.

Consider this: Six years ago, $30 billion sat in U.S. leveraged ETFs – the type of instrument that allows investors to make turbo-charged bets on the market.

Today, they just hit a record $177 billion. That’s nearly six times more money, making bigger and more aggressive bets.

Investors are sprinting full-speed into the stock market. And it’s not just Americans…

Foreign investors now hold a record $21 trillion in U.S. stocks – up 170% since 2020. They have an unusually large share of their money in U.S. stocks – more than even during the peak of the dot-com bubble.

In other words, the entire world is piling into American stocks.

Meanwhile, the S&P 500 just hit a fresh all-time high, adding $11 trillion of value in just seven weeks.

This is what a Melt Up looks like.

I know what the skeptics will say: “This sounds like a top.”

But here’s what they’re missing…

Every bull market in history – 1929, the dot-com boom, Japan in the late ’80s, and more – followed the same exact pattern.

Stocks rise steadily for years… Then, something changes. People who sat on the sidelines panic that they’re missing out. They rush in all at once… prices explode… and then, when there’s nobody left to buy… it all comes crashing down.

We’re not at peak euphoria yet. Not even close. You’ll know it arrives when your neighbors and barber are giving you stock picks.

But Melt Ups happen fast. During the dot-com bubble, the Nasdaq nearly doubled in just a few months.

The window is still open – for now.

That’s why I just published a brand-new presentation laying out everything you need to know to maximize your returns during the Melt Up (including how to know when to get out before the Melt Down).

Watch it right here while there’s still time.

Regards,

Brett Eversole

Senior Editor & Analyst, Stansberry Research

P.S. If you’re over 55, navigating the next 12 to 18 months in the markets will be the final, most important decision of your financial life – the difference between the retirement you’ve planned for… and one haunted by “what ifs.” You deserve to be on the right side of it.

Click here to learn the simple steps I’m urging my readers to take before it’s too late.

FEATURED

Copper and Uranium in 2026: Supply Still Feels Tight

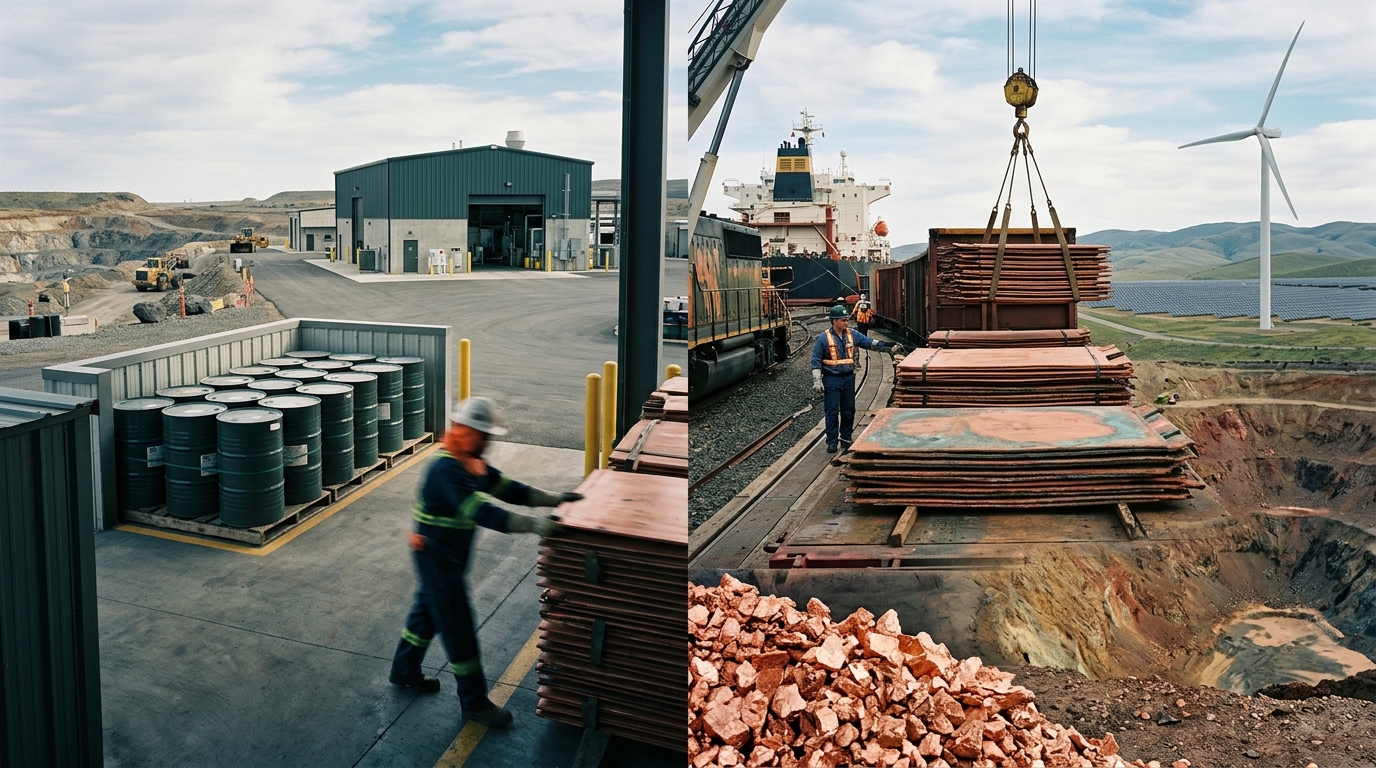

Copper at six bucks and change is the kind of number that makes people suddenly remember what “input cost” means.

COMEX copper was about $6.37 per pound on May 29, 2026. Not a typo. That’s after it pushed to fresh highs earlier in May and then cooled off a bit. ([tradingeconomics.com](https://tradingeconomics.com/commodity/copper?utm_source=openai))

And uranium is doing the thing uranium always does: the day to day quote gets all the attention, while the longer term contracting cycle does the real work in the background.

Here’s the thing. A lot of commentary on copper leans on one clean line: “we’re in deficit.” Sometimes that’s true. Sometimes it’s a story people repeat because it’s convenient.

The International Copper Study Group table that’s been circulating recently shows a 2025 refined copper balance of +462 thousand metric tons. That’s a surplus, at least in that framework. ([icsg.org](https://icsg.org/wp-content/uploads/Table1.pdf?utm_source=openai))

So if you’ve been using “2025 deficit of 289,000 tons” as a pillar for the thesis, I’d drop it unless you can point to the exact report and date that supports it. This matters, because people trade off these numbers like they’re gospel. They’re not.

What’s interesting is that a paper surplus doesn’t automatically mean the market feels loose. You can still get real friction when metal is in the wrong place, in the wrong form, or locked up by someone who’s not selling. That’s when price can look “too high” for longer than it should.

Your Download Link (Expiring)

If you still haven’t downloaded the free Simple Options Trading For Beginners guide…

…please take a few seconds and download it right now before your download link expires.

I eventually plan to charge money for this report, so do yourself a favor and download it now…

That way, no matter what it costs in the future, you’ll have a free copy on your computer.

Make sense?

Simple Options Trading For Beginners (Download Link Expires)

Slight tangent, but it matters: every cycle has a moment where the buyer stops arguing about price and starts arguing about delivery dates. Copper feels closer to that kind of moment than people want to admit.

Now zoom in on the equities for a second.

FCX tends to behave like “copper beta plus operational execution.” SCCO tends to behave like “copper beta plus capital return expectations.” Same general driver, different personality. If copper holds up, the conversation shifts quickly from earnings to what management does with the cash.

On uranium, I wanted to clean up one specific thing because it’s easy to get sloppy here.

Cameco’s Q1 2026 release shows revenue of about $845 million (vs $789 million in Q1 2025). ([nasdaq.com](https://www.nasdaq.com/press-release/cameco-reports-first-quarter-2026-results-financial-results-and-operational-execution?utm_source=openai))

Also, for 2026 guidance, the language being repeated around the quarter is: delivery guidance of 29 to 32 million pounds, production targets of 19.5 to 21.0 million pounds, and market purchases up to 3 million pounds. ([investing.com](https://www.investing.com/news/company-news/cameco-q1-2026-slides-uranium-output-on-track-eps-beats-forecast-93CH-4679186?utm_source=openai))

The part people skip is how these uranium businesses are built to manage obligations over time, not to “win the quarter.” When utilities move to secure long term supply, it changes the whole tone of the market. It just doesn’t always show up cleanly in a single spot quote.

The New Arms Race Is Being Built Right Now

Global tensions are accelerating a new kind of arms race powered by advanced technology.

AI, drones, and autonomous systems are becoming central to modern defense strategies. This report reveals five companies positioned to benefit from this shift and what it could mean for investors.

If you’re approaching this through options, my bias is simple: keep it defined risk, keep it small, and avoid the temptation to get cute with timing. Commodity linked stocks can make you look right and still hurt you.

- Watch how volatility behaves into earnings windows and guidance updates

- Pay attention to where open interest clusters on the liquid names

- Be honest about what you need: a move, or time passing

Tickers people keep circling in this space: CCJ, UEC, FCX, SCCO, and COPX.

Worth a look: pull up that ICSG balance table and sit with it for two minutes. Then look at where copper actually traded on May 29. If those two things feel like they’re saying different things, that’s the point. ([icsg.org](https://icsg.org/wp-content/uploads/Table1.pdf?utm_source=openai))

I’ll be watching whether copper can stay above $6 into early June without the market getting shaky about growth again. And on uranium, I’m watching the contract headlines more than the daily number. It’s not as flashy, but it’s usually the real driver.

Take a closer look, and tell me what you think is being missed.